Demonetisation Impact – Where should you invest your idle money?

Demonetisation Impact – Where should you invest your idle money?

5 min to read

5 min to read

In our latest endeavour to help the jewellers and diamantaires adapt to the changing financial scenarios in the country post demonetisation, this article aims to provide an understanding regarding investment opportunities from underutilised surplus in bank accounts.

The unprecedented decision of the Government of India to withdraw high denomination notes and the subsequent withdrawal limits has left all of us with lot of idle money lying in our bank accounts. As we all know, that the our money lying the savings bank account fetches us barely 2-3% post tax returns. This leaves us with the question is where should we invest our idle money where we can get good post tax returns. The immediate answer that one has is investing the money in fixed deposits. However as one is aware, due to the large deposits received by the banks, they have reduced the deposit rates substantially. Further, the fixed deposits come with a fixed tenure, and early redemption shall lead to penal charges.

Apart from fixed deposits, there are several other alternatives to invest your idle money and earn better returns without compromising on liquidity or taking too much risk. Which one is the best for you shall depend upon the following factors

1. Tenure of investment – For how long you can invest your money

2. Taxation – What is the taxability of the income you earn

Based upon the above parameters and your appetite to take little risk you can consider the following options to invest your money.

1. Liquid Funds and ultra short term funds – Liquid funds and ultra short term funds primarily invest in very short term debt securities and only a small portion in long term debt securities. These funds are relatively safe schemes and shall generate an annualised returns of 6.5% – 7.5% p.a. Further unlike fixed deposits, interest earned on such funds is not treated as interest income but is taxable as capital gains and shall be eligible for indexation benefit if it is held for a period of 3 years. Further it is also worthwhile to note that there is no TDS that is deducted on gains earned through mutual funds.

One of the other benefits of liquid and ultra short term funds is that some funds like Reliance Money Manager Fund, DSP Blackrock Money Manager Fund and Birla Sunlife Cash Manager fund provide the facility of instant redemption of upto Rs. 2,00,000. This important feature provides the investor the benefit of redeeming the money only when required thus enabling them to earn the extra interest. In the case of other ulta-short term funds also the money is relatively easy to redeem. If the redemption request is placed before 2.30 pm the money is credited in the bank account next day morning before 10.30 am.

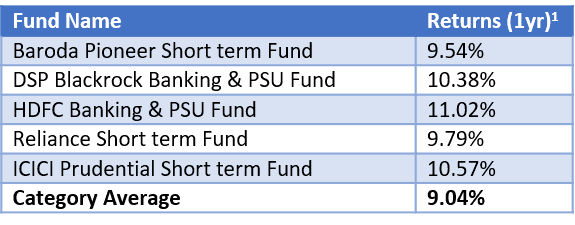

2. Short term Fund – A short term investment fund is a type of fund which primarily invest in money market and debt securities largely in short and medium term bonds which have a higher duration resulting in a return higher than ultra-short term funds. These funds are recommended for those who do not require their money for a period of 3 months to 1 year. With the interest rates on fixed deposits in a downward trend, these funds offer better returns compared to fixed deposits over a one year period. The post tax returns shall be substantial if one holds on to the investment for a period of 3 years. The redemption and taxation of income from short term funds is similar to income received from ultra-short term funds.

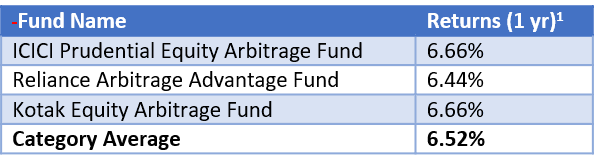

3. Arbitrage Funds – Investors who are uncertain on their investment horizon can also look at arbitrage funds provided their investment duration is more than a month. Arbitrage funds do not carry substantial risk like equity funds since the investments in equity is hedged by having positions in the derivative market. Hence they generate stable returns which are in the range of 5.5% to 7% p.a. The investor can claim tax benefit by investing in dividend options of arbitrage funds since they are tax free. However, if the investor is willing to invest for a period of more than 1 year, he should consider the growth option since investments in equity funds is tax free after one year.

4. Accrual Funds/Credit Opportunities – Investors who are looking at investing their money for more than 1 year can look at this category of funds. Accrual/Credit Opportunities fund invest in long term corporate bonds which carry higher interest rates. These funds benefit from the higher interest rates accruing on these bonds as well as the capital gains accruing from higher prices on account of trading in these long-term bonds in the secondary market. These funds are best suited for those who usually park their money in fixed deposits or have higher holding capacity, since they provide you with tax advantage along with superior returns which makes the post tax returns better than fixed deposits.

Summary Chart

Example of indexation benefit*

To conclude, mutual funds provide a variety of products where one can consider investing based upon the investment horizon. As can be seen from the discussion above, these products offer better returns than fixed deposits. Although the above products are not completely risk free, the risk in these funds can be mitigated with the help of choosing the right product for your risk appetite and investment horizon.

About the Author

Dhruv Rawani, Managing Partner at Vitta Advisors LLP specialises in providing financial advisory services. Boosting a client base of more than 600 individual clients successfully served over the last 18 years, their platform of products and services provides access to a robust range of investing and wealth building tools with personal guidance from them at a convenient time right at your doorstep. Vitta Advisors LLP help you understand your financial objectives and making appropriate plans to realise them through financial planning, asset allocation and investment monitoring. You can get in touch with Dhruv on +91 97731 64338 or email on dhruv.rawani@vittaadvisors.com

* ICICI Regular Savings Fund returns are calculated post indexation benefits. Traditional investment returns are calculated assuming highest tax rate. Past performance may or may not be sustained in the future. Returns are calculated on annualised basis.

Returns calculated for 1 year period as on November 2016 based on data from Value research.

Disclaimer

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. There can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. Neither J K Diamonds Institute nor Vitta Advisors LLP is responsible for any action taken based on above information.

In our latest endeavour to help the jewellers and diamantaires adapt to the changing financial scenarios in the country post demonetisation, this article aims to provide an understanding regarding investment opportunities from underutilised surplus in bank accounts.

The unprecedented decision of the Government of India to withdraw high denomination notes and the subsequent withdrawal limits has left all of us with lot of idle money lying in our bank accounts. As we all know, that the our money lying the savings bank account fetches us barely 2-3% post tax returns. This leaves us with the question is where should we invest our idle money where we can get good post tax returns. The immediate answer that one has is investing the money in fixed deposits. However as one is aware, due to the large deposits received by the banks, they have reduced the deposit rates substantially. Further, the fixed deposits come with a fixed tenure, and early redemption shall lead to penal charges.

Apart from fixed deposits, there are several other alternatives to invest your idle money and earn better returns without compromising on liquidity or taking too much risk. Which one is the best for you shall depend upon the following factors

1. Tenure of investment – For how long you can invest your money

2. Taxation – What is the taxability of the income you earn

Based upon the above parameters and your appetite to take little risk you can consider the following options to invest your money.

1. Liquid Funds and ultra short term funds – Liquid funds and ultra short term funds primarily invest in very short term debt securities and only a small portion in long term debt securities. These funds are relatively safe schemes and shall generate an annualised returns of 6.5% – 7.5% p.a. Further unlike fixed deposits, interest earned on such funds is not treated as interest income but is taxable as capital gains and shall be eligible for indexation benefit if it is held for a period of 3 years. Further it is also worthwhile to note that there is no TDS that is deducted on gains earned through mutual funds.

One of the other benefits of liquid and ultra short term funds is that some funds like Reliance Money Manager Fund, DSP Blackrock Money Manager Fund and Birla Sunlife Cash Manager fund provide the facility of instant redemption of upto Rs. 2,00,000. This important feature provides the investor the benefit of redeeming the money only when required thus enabling them to earn the extra interest. In the case of other ulta-short term funds also the money is relatively easy to redeem. If the redemption request is placed before 2.30 pm the money is credited in the bank account next day morning before 10.30 am.

2. Short term Fund – A short term investment fund is a type of fund which primarily invest in money market and debt securities largely in short and medium term bonds which have a higher duration resulting in a return higher than ultra-short term funds. These funds are recommended for those who do not require their money for a period of 3 months to 1 year. With the interest rates on fixed deposits in a downward trend, these funds offer better returns compared to fixed deposits over a one year period. The post tax returns shall be substantial if one holds on to the investment for a period of 3 years. The redemption and taxation of income from short term funds is similar to income received from ultra-short term funds.

3. Arbitrage Funds – Investors who are uncertain on their investment horizon can also look at arbitrage funds provided their investment duration is more than a month. Arbitrage funds do not carry substantial risk like equity funds since the investments in equity is hedged by having positions in the derivative market. Hence they generate stable returns which are in the range of 5.5% to 7% p.a. The investor can claim tax benefit by investing in dividend options of arbitrage funds since they are tax free. However, if the investor is willing to invest for a period of more than 1 year, he should consider the growth option since investments in equity funds is tax free after one year.

4. Accrual Funds/Credit Opportunities – Investors who are looking at investing their money for more than 1 year can look at this category of funds. Accrual/Credit Opportunities fund invest in long term corporate bonds which carry higher interest rates. These funds benefit from the higher interest rates accruing on these bonds as well as the capital gains accruing from higher prices on account of trading in these long-term bonds in the secondary market. These funds are best suited for those who usually park their money in fixed deposits or have higher holding capacity, since they provide you with tax advantage along with superior returns which makes the post tax returns better than fixed deposits.

Summary Chart

Example of indexation benefit*

To conclude, mutual funds provide a variety of products where one can consider investing based upon the investment horizon. As can be seen from the discussion above, these products offer better returns than fixed deposits. Although the above products are not completely risk free, the risk in these funds can be mitigated with the help of choosing the right product for your risk appetite and investment horizon.

About the Author

Dhruv Rawani, Managing Partner at Vitta Advisors LLP specialises in providing financial advisory services. Boosting a client base of more than 600 individual clients successfully served over the last 18 years, their platform of products and services provides access to a robust range of investing and wealth building tools with personal guidance from them at a convenient time right at your doorstep. Vitta Advisors LLP help you understand your financial objectives and making appropriate plans to realise them through financial planning, asset allocation and investment monitoring. You can get in touch with Dhruv on +91 97731 64338 or email on dhruv.rawani@vittaadvisors.com

* ICICI Regular Savings Fund returns are calculated post indexation benefits. Traditional investment returns are calculated assuming highest tax rate. Past performance may or may not be sustained in the future. Returns are calculated on annualised basis.

Returns calculated for 1 year period as on November 2016 based on data from Value research.

Disclaimer

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. There can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. Neither J K Diamonds Institute nor Vitta Advisors LLP is responsible for any action taken based on above information.

.

.

CONTACT US

+91 9892779365 ,

+91 9619057706

contact@jkdiamondsinstitute.com

1104, Hubtown Solaris, Andheri (E), Mumbai – 400069

CONTACT US

+91 9892779365 ,

+91 9619057706

contact@jkdiamondsinstitute.com

1104, Hubtown Solaris, Andheri (E), Mumbai – 400069